Over the past decade, the Belt and Road Initiative has evolved into a pivotal engine for global connectivity and infrastructure investment. As transcontinental projects in transportation, energy, and urban development accelerate, construction aggregates—an indispensable foundational material, are both witnessing and enabling a profound reshaping of the global construction landscape and its industrial value chains. This article examines the new landscape, emerging challenges, and unfolding opportunities for the sand and aggregates industry in the context of the Belt and Road.

Macro Background Of Global Infrastructure Wave And Demand For Sand And Gravel Aggregates

Global Influence of the Belt and Road Initiative

Since its launch in 2013, the Belt and Road Initiative (BRI) has expanded to encompass 150+ countries and international organizations across Asia, Europe, Africa, and the Middle East, becoming a key platform for global economic cooperation and infrastructure connectivity.

Within this trajectory, infrastructure construction has created a pronounced, inelastic demand for construction aggregates. As the foundational material for highways, railways, ports, and large-scale urban complexes, aggregates are direct beneficiaries of the rapid upswing in global infrastructure investment.

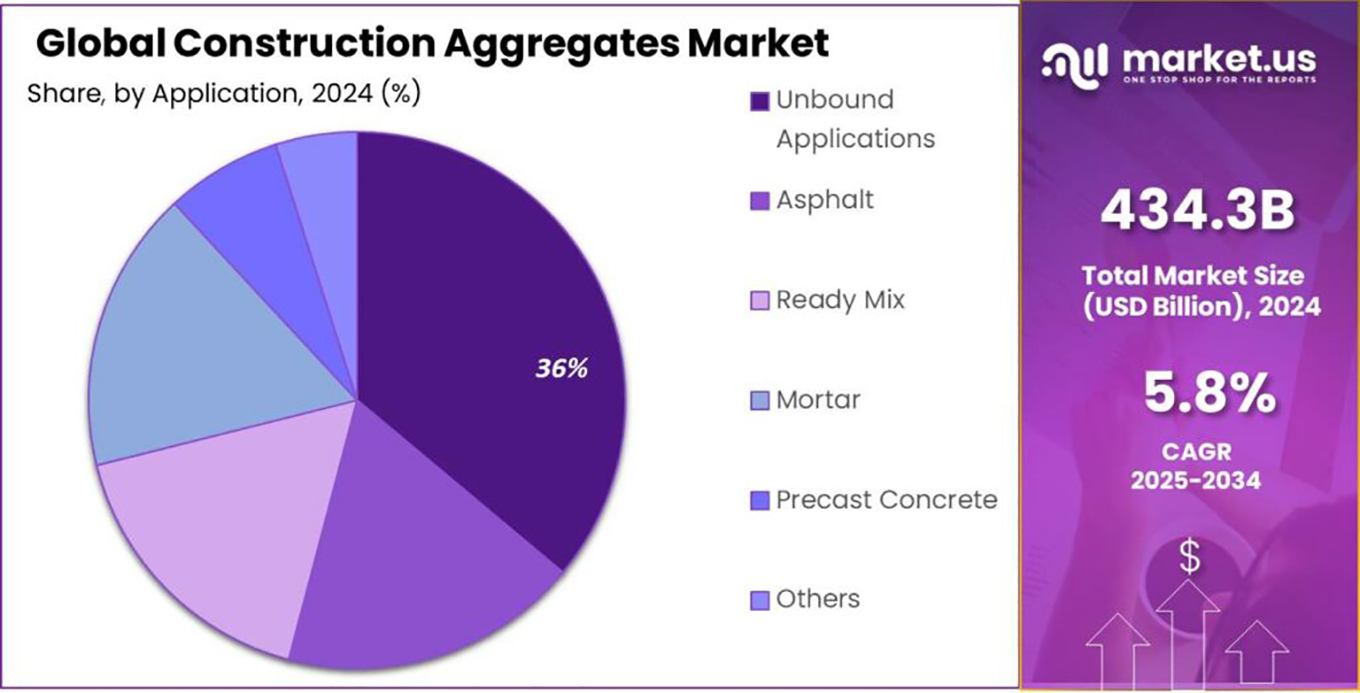

The Basic Structure Of The Global Aggregates Market

Aggregates are the world’s largest by volume and most widely consumed construction material. According to UNEP, global aggregate output is approximately 44 billion tonnes, with major producers and consumers including China, the United States, India, Turkey, and others. Yet the sand and aggregate production industry remains highly localized: over 90% of supply serves domestic markets, and cross‑border trade accounts for less than 5%. This is driven by several defining characteristics of the sector:

- Strong geographic specificity: Resources are widely distributed and typically mined and consumed locally.

- Localized supply chains: High transportation costs constrain long-range circulation.

- High sensitivity to infrastructure demand: Economic cycles and infrastructure investment directly shape industry volatility.

Market Characteristics And Demand Potential For Aggregates Across Key Belt And Road Regions

The Belt and Road spans countries and regions with diverse development stages, resource endowments, and policy environments, resulting in a heterogeneous aggregates market landscape. Key regional profiles are as follows:

Southeast Asia: Dense Planning, Strong Investment

- Indonesia: The 2025–2045 National Long-Term Development Plan positions infrastructure as a pillar, with unprecedented investment over the next two decades.

- Vietnam: The 2021–2030 Transport Infrastructure Network Plan targets 5,000 km of new expressways and multiple international hub ports.

- Philippines: Successor projects under Build, Build, Build continue to accelerate, with infrastructure investment sustaining annual growth above 7%.

Urbanization has accelerated in Indonesia, Vietnam, Malaysia, and the Philippines, underpinning robust infrastructure spending. However, tensions between resource extraction and ecological protection are intensifying. Restrictions on coastal and river sand mining are pushing the sector toward greener extraction and increased adoption of manufactured sand.

Central Asia: Resource-rich, capability to be upgraded

Kazakhstan and Uzbekistan possess abundant aggregates resources across vast territories but have relatively weak processing and equipment capabilities. The rollout of Central Asia transport corridors and energy transmission projects is expanding local markets. Inflows of foreign capital and international technology are pivotal to industry modernization.

Middle East: Ambitious Visions, Front‑Loaded Megaprojects

- Saudi Arabia: Under Vision 2030, giga-projects such as NEOM and the Red Sea development are expected to exceed USD 1 trillion in total investment.

- UAE: Dubai’s 2040 Urban Master Plan envisions doubling the city’s urban area, implying substantial new-build volumes.

Demand for aggregates remains elevated. Stringent requirements on raw material quality and environmental standards are driving widespread adoption of green mining practices and intelligent equipment.

Africa: Large Gap, Significant Upside

- Funding needs: According to the African Development Bank, to meet basic development requirements, Africa faces an annual infrastructure financing gap of USD 130–170 billion.

- Demand focus: Transport networks (roads, railways) and energy-water infrastructure (dams, grids) account for over 60% of aggregates consumption.

Countries such as Kenya, Ethiopia, and Nigeria confront acute infrastructure deficits. Investment in roads, railways, and ports is growing at roughly 13%, underscoring sizable market potential for aggregates. Logistics bottlenecks and limited local supply capacity are catalyzing foreign-local partnerships and supply chain upgrading.

South Asia: High Population Density And Supply Chain Frictions

India, Bangladesh, and Pakistan exhibit dense populations, rapid urbanization, and strong infrastructure demand. India’s aggregates demand reached 640 million tonnes in 2023, up 8% year on year. Nonetheless, policy volatility and supply chain inefficiencies continue to constrain sector development.

Reshaping The Global Aggregates Supply Chain And Emerging Regional Cooperation Models

Constraints Of Traditional Supply Chains: The “Short-Radius” Dilemma And Global Imbalances

Prior to the Belt and Road Initiative (BRI), the global aggregates supply chain was characterized by extreme localization:

Transport Radius Constraints

Aggregates are high-density, low-value commodities; overland logistics can account for more than 40% of delivered cost. As a result, over 90% of transactions occur within roughly 150 km of the quarry, and cross-border trade represents less than 1% of global output.

Regional Supply-demand Disconnects

Emerging markets in Southeast Asia and Africa often face “demand without supply” due to lagging local mine development, while parts of Central Asia and the Middle East, though resource-rich, rely on imports of high-quality manufactured sand because of gaps in processing technology.

This legacy model, predominantly local self-sufficiency with minimal cross-border flows, has increasingly revealed efficiency bottlenecks under the BRI’s surge in large-scale infrastructure demand.

BRI-Driven Supply Chain Transformation: Three Innovation Archetypes

Regionalized supply networks

Leveraging geographic proximity and resource complementarity, BRI economies are building regional aggregates “supply clusters.” Examples include Turkey supplying the Balkans and Kazakhstan serving neighboring Central Asian markets. These networks, underpinned by geographic adjacency, complementary resources, and policy coordination, help stabilize intra-regional supply and ease single-country pressure.

Cross-border investment and joint development

The BRI is catalyzing global capital and technology to converge on aggregates along the route, forming three typical cooperation models: foreign participation in local quarry development, end-to-end value chain collaboration, and local–foreign joint ventures. Such partnerships address funding and technology gaps in resource countries while opening incremental markets for investors. Deloitte (2023) notes that cross-border aggregates projects along the BRI deliver average returns 2–3 percentage points higher than traditional sectors.

Project-centric supply chains

For mega cross-border projects, railways, ports, industrial parks, countries are piloting “project-dedicated supply chains,” embedding aggregates supply into full lifecycle project management to enhance efficiency and assurance.

Cross-Border Cooperation And Investment Trends

Foreign Capital Inflows

Investors from China, Türkiye, the Gulf, and Europe are accelerating deployments in BRI countries, directly investing in quarries and processing plants or aggregating resources via project-based partnerships.

EPC and BOT integration

Large infrastructure programs increasingly adopt EPC (engineering, procurement, and construction) and BOT (build–operate–transfer) models. Aggregates supply is planned as part of one-stop solutions, enabling centralized procurement and efficient delivery.

Technology and equipment partnerships

Leading global manufacturers in rock crushing and screening, alongside environmental technology firms, are entering emerging markets, advancing green, digital, and intelligent upgrades across the local industry.

The BRI is propelling the global aggregates sector from a closed, siloed system toward openness and collaboration, lifting overall efficiency and sustainability.

Future Trends: Greening, Digitization and Global Collaboration

Under the continued momentum of the Belt and Road Initiative, the global sand and aggregate industry is at a pivotal moment of transformation and upgrade. Over the next decade the sand and aggregate will accelerate change around three core directions,green production, intelligent upgrades and deepened global collaboration, shaping a more sustainable, efficient and inclusive international industrial ecosystem. This evolution not only concerns the survival and competitiveness of the aggregates industry itself, but also underpins coordinated progress in global infrastructure delivery and ecological protection.

Accelerating Green, Smart and Standardized Development

- Regulatory drivers: Major markets, including the EU, Southeast Asia and Africa, are introducing mandatory requirements: the EU sets a carbon-intensity cap for aggregate production (no more than 40 kg CO₂ per tonne); Indonesia requires mine wastewater recycling rates above 85%; South Africa mandates that mines set aside ecological protection zones.

- Technological innovation: Operators are rapidly adopting low-carbon technologies, water-circulation systems and ecological restoration techniques.

- Standards harmonization: International bodies (for example ISO) are developing global green aggregate standards and facilitating mutual recognition of certifications, such as the EU “Green Label” and China’s “Three-Star Mine”—to ease cross-border trade in aggregate products.

Intelligentization: Digital Technologies Reshape Production And Supply Chains

- Production intelligence: Intelligent mines use drone-based modeling and sensor networks to optimize extraction and safety monitoring; smart production lines automatically adjust parameters to improve throughput and product quality.

- Logistics intelligence: Smart logistics systems cut empty-run rates; digital platforms connect the entire “pit-to-plant-to-site” chain to enable demand forecasting and real-time inventory management.

Global Collaboration: Resource Complementarity and a Shared Destiny

- Resource and technology cooperation: Resource-rich countries (e.g., Kazakhstan) supply ore to demand markets (e.g., Vietnam) and co-develop cross-border processing hubs; technology-leading countries (e.g., Germany, China) export green processes and smart equipment through “technology transfer centres.”

- Standards and rules alignment: ASEAN is advancing regional uniformity in aggregate quality standards; the African Union is working to incorporate local grading standards into the international system, addressing supply disruptions caused by cross-border standard mismatches.

Driven together by green technologies, intelligent tools and global cooperation, the aggregates industry of the future will reliably supply sustainable materials for Belt and Road infrastructure, while contributing to climate action and narrowing development gaps worldwide.

Recommendations for Global Aggregates Industry Participants

Investors and Developers

— focus on regional potential and stringent compliance and environmental risk control

- Target selection: Prioritise Belt and Road corridors with intensive infrastructure investment—Southeast Asia (e.g., Indonesia’s new capital, Vietnam’s highway networks), the Middle East (e.g., Saudi NEOM), and Africa (e.g., trans-regional transport corridors). Align market entry timing and modalities with national development plans and projected aggregates demand.

- Reinforce risk mitigation: Make local partnerships (e.g., joint ventures with resource-country firms), regulatory compliance and environmental responsibility core investment criteria to reduce risks from policy shifts, environmental penalties and community conflicts.

Aggregates Producers

— upgrade processes and supply chains; integrate into global project chains

- Improving quality and efficiency on the production side: Focus on enhancing the environmental friendliness and efficiency of production processes, and explore opportunities for cross-border supply or regional cooperation to expand market coverage.

- Deepen supply-chain collaboration: Proactively engage EPC contractors, sovereign and institutional investors by securing long-term supply contracts or co-investing in integrated pit-to-plant projects to embed into major infrastructure supply chains and stabilise order flow and margins.

Equipment and Technology Suppliers

— meet differentiated demand and strengthen local services

- Regional product and technology adaptation: Offer tailored solutions that meet rising demand for high-efficiency, energy-saving equipment (electric crushing plants, solar-powered systems) and low-environmental-impact designs (low-noise, low-dust).

- Build local service capability: Deliver technical transfer (e.g., training on intelligent control systems, O&M support) and establish local service networks (after-sales centres and parts warehouses in resource countries). Such local presence lowers customer adoption barriers and is critical to capture emerging market share.

The Belt and Road Initiative presents a historic opportunity for infrastructure development and a broad stage for the global aggregates industry to optimize resources, deepen technical cooperation and accelerate green transformation. Industry stakeholders must intensify dialogue, deepen partnerships and share responsibilities to realize mutual gains and build an open, green, efficient and inclusive new paradigm for the global sand and aggregate sector.